Key points

- Snowflake is a rapidly growing data warehouse solutions provider that enables businesses to store, manage and analyze their data in a centralized, cloud-based location.

- Snowflake shares fell more than 20% on fiscal 2025 forecasts and the sudden replacement of CEO Frank Slootman.

- The new CEO, Sridhar Ramaswamy, was former vice president of artificial intelligence and search at Google and purchased over $5 million in Snowflake stock through his trust, as disclosed on March 27, 2024.

- 5 stocks we like better than Snowflake

Snowflake Inc. NYSE: SNOW is a cloud-native data warehouse in the IT and technology industry, offering cloud-based data platform as a service (PaaS) solutions to businesses. Snowflake shares plunged more than 20% on the release of its fiscal fourth-quarter 2024 earnings. Despite beating consensus estimates, it delivered a gut punch with the surprise retirement of its CEO of 5 years, Frank Slootman, and soft fiscal guidance for 2025.

The new CEO can be a user in the age of artificial intelligence for Snowflake

Its new CEO, Sridhar Ramaswamy, was senior vice president of AI and research at Alphabet Inc. NASDAQ:GOOGL, owned by Google. CEO Slootman has often been criticized for falling behind in integrating and offering artificial intelligence (AI) features and tools. Appointing an experienced AI executive to usher in the AI era for Snowflake is a bullish move. Former CEO Slootman will remain chairman of the board. On March 27, 2024, CEO Ramaswamy disclosed the purchase of nearly $5 million worth of stock or 31,542 shares at $158.52 in an SEC filing. This brings the total ownership of his Ramaswamy Trust to 224,181 shares.

Centralized data warehouse

Snowflake is a one-stop shop to store, manage, and analyze massive amounts of data efficiently and scale elastically within Snowflake’s cloud infrastructure. Amazon.com Inc. NASDAQ: AMZN, AWS, Microsoft Co. NASDAQ: MSFT and Google Cloud. Snowflake customers can leverage artificial intelligence (AI) and machine learning (ML) within the data platform with data sharing capabilities, scalable infrastructure, and the ability to integrate with popular AI and ML frameworks. Check the heat map of the sector on MarketBeat. Obtain AI-powered insights on MarketBeat.

Blazing growth

Snowflake reported fiscal fourth-quarter 2024 earnings per share of 35 cents, beating analysts’ consensus estimates of 18 cents by 17 cents. Revenue increased 32% year-over-year to $774.7 million versus consensus estimates of $761.04 million. Its remaining performance obligations (RPO) increased 41% year over year to $5.2 billion. Net revenue retention rate was 131% in the quarter. It brought its end-customers over the past 12 months with more than $1 million in product revenue to 461, up 39% year-over-year. The company serves 691 of the Forbes Global 2000 companies as customers, up 8% year over year.

Soft tax guidance for 2025

Snowflake expects first-quarter fiscal 2025 product revenue of $745 million to $750 million, or growth of 26% to 27%. Non-GAAP operating margins are expected to be around 3%. Full-year fiscal 2025 revenues are expected to grow 22% to $3.25 billion. This is down from the 38% growth rate for full-year 2024. Non-GAAP operating margins are expected to be around 6%, down 200 basis points.

Former CEO and President Slootman commented, “Snowflake ended fiscal 2024 with product revenue growth of 38% year-over-year, totaling $2.67 billion. Adjusted free cash flow non-GAAP was $810 million, representing 56% year-over-year growth.” Slootman concluded, “We are successfully waging a campaign against the largest companies globally as more companies and institutions make data Snowflake Cloud is the platform for their AI and data strategy.”

Analyst actions

Analysts were busy with ratings and price target changes. On February 29, 2024, Morgan Stanley cut its rating from Overweight to Equal-Weight and lowered its price target to $175, from $230. Macquarie upgraded SNOW to Outperform from Neutral. HSBC Securities downgraded SNOW to Reduce from Hold. On March 15, Guggenheim upgraded SNOW to Neutral from Sell. On March 18, 2024, Mooness, Crespi & Hardt moved to Neutral from a Sell rating. On March 19, 2024, Redburn Atlantic downgraded shares of SNOW to Sell from Neutral, cutting its price target to $125 from $180.

Snowflake analyst ratings and price targets I’m on MarketBeat. Snowflake peers and competitor actions can be found with MarketBeat Stock Screener.

Daily rounded fund

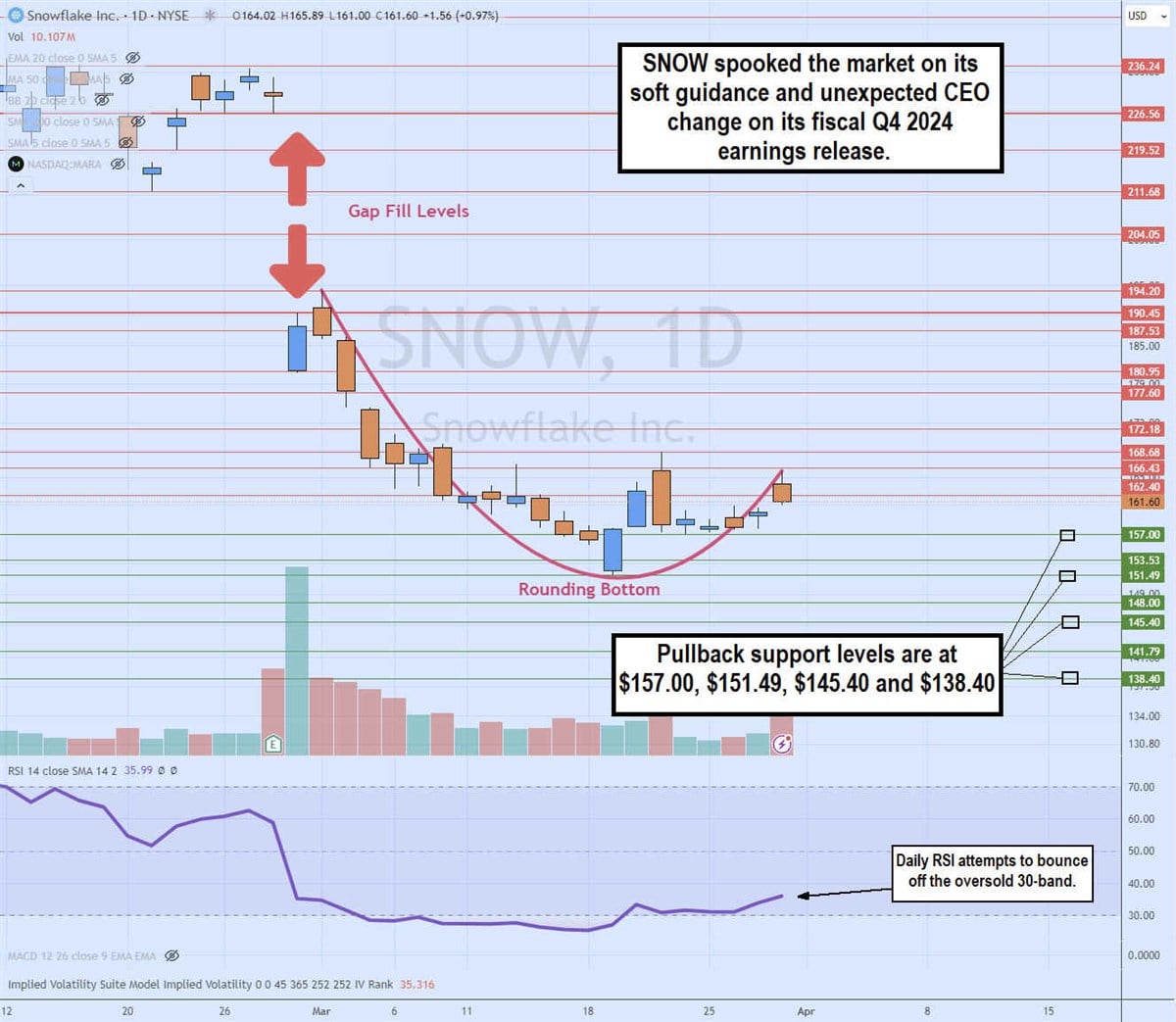

The daily candlestick chart for SNOW illustrates a rounded bottom pattern. SNOW fell from $226.56 to $194.20 based on its soft guidance and the sudden and unexpected CEO change announced during its fiscal fourth quarter 2024 earnings release on February 29, 2024. Shares continued to decline until to a low of $151.49 on March 19, 2024. A rounded bottom formed off the lows as stocks attempted to rally, fueled by the daily relative strength index (RSI) bouncing around the 30 band. The pullback support levels they are at $157.00, $151.49, $145.40 and $138.40.

Before you consider Snowflake, you’ll want to hear it.

MarketBeat tracks Wall Street’s highest-rated and best-performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market takes hold… and Snowflake wasn’t on the list.

While Snowflake currently has a “Moderate Buy” rating among analysts, top-rated analysts believe these five stocks are better buys.

View the five stocks here

Wondering what the next big-hitting stocks with solid fundamentals will be? Click the link below to learn more about how your portfolio could blossom.

Get this free report