Key points

- Lyft reported strong earnings in the fourth quarter of 2023, beating EPS expectations by 11 cents on 17% year-over-year bookings growth.

- Lyft saw a 47% increase in driving hours by drivers because it guaranteed that drivers would earn 70% of the total fares paid by riders before outside commissions or would make up the difference.

- Lyft expects to generate positive full-year free cash flow for the first time in its history in 2024, which sets the stage for profitability.

- 5 Stocks We Like Better Than Lyft

Rideshare operator Lyft Inc. NASDAQ:LYFT the stock got a second life thanks to its fourth-quarter 2023 earnings performance. The computer and technology company was considered a distant second in the rideshare sector dominated by Uber Technologies Inc. NYSE:UBER. Under new leadership led by CEO David Risher, former Amazon.com Inc. NASDAQ: AMZN AND Microsoft Co. NASDAQ:MSFT, Lyft appears to be back on a renewed path to profitability. There’s no arguing that Lyft’s business is still growing, as highlighted by the 17% year-over-year growth in bookings despite stable revenue.

The oligopoly continues

Markets have realized that even though Uber has taken the lead, Lyft is still the (distant) No. 2 in the industry, which is still an oligopoly. Oligopolies are still rampant in trade. Although not exactly a uniform oligopoly The Boeing Co. NYSE: BA and Airbus with airliners or The Coca-Cola Co. NYSE: KO AND PepsiCo Inc. NASDAQ:PEP with drinks. Uber and Lyft’s oligopoly is more similar Alphabet Inc. NASDAQ:GOOGL owned Google and Microsoft Co. NASDAQ:MSFT owned Bing, which represents the oligopoly in Internet search.

Get back on track

On February 13, 2024, Lyft released fourth-quarter 2023 results for December 2023. The company reported adjusted earnings per share (EPS) of 19 cents, excluding non-recurring items, beating consensus analyst estimates by 8 cents . 11 cents. Net loss was $26.3 million compared to $588.1 million a year earlier. The net loss includes $93.3 million in stock-based compensation related to payroll taxes. Adjusted EBITDA was $66.6 million compared to a loss of $248.3 million in the same period a year earlier. It beats estimates by $50 million to $55 million. Revenue was unchanged at $1.2 billion versus analysts’ $1.22 billion estimate.

Record runners and gross bookings

Active cyclists grew 10% year-on-year. Gross bookings increased 17% year over year. Gross passengers and bookings reach all-time highs for the company. Rides grew 26% year over year to 191 million. Full-year rides increased 10% to 709 million. Total active riders for the full year rose to more than 40 million, the highest annual ridership in Lyft’s history.

Promise of punctual collection

Lyft has introduced its on-time pickup promise for scheduled airport rides in major markets. This initiative promises passengers that their driver will pick them up within 10 minutes of their scheduled pickup time, or they will receive $100 in Lyft ride credits. As a result, 98% of scheduled airport trips were on time, reaching an all-time high.

Women+ Connect shows strong growth

Lyft’s Women+ Connect feature has had nearly 7 million rides to date. This feature prioritizes matching female passengers with women and non-binary drivers. Over 67% of eligible drivers chose to keep the feature active 99% of the time.

Lyft Media is getting noticed

Lyft’s in-app video ads launched in the fourth quarter with strong results measured in views and clicks. The company is working closely with partners to create great experiences for cyclists, leveraging its lifestyle and destination targeting capabilities. Nearly 20% of Lyft rides have a direct connection to one of its partners. These partnerships translate into collaboration agreements and advertising on its app. Some of the partnerships include Delta Air Lines Inc. NYSE: FROM, Comcast Co. NASDAQ: CMCSK owned by Universal Pictures, Starbucks Co. NASDAQ: SBUX, Amazon.com Inc. NASDAQ: AMZN AND The Apple company. NASDAQ:AAPL. Obtain AI-powered insights on MarketBeat.

Lyft increases forward driving

Lyft expects gross bookings for the first quarter of 2024 to be between $3.5 billion and $3.6 billion. Adjusted EBITDA is expected to be between $50 million and $55 million, with an adjusted EBITDA margin between 1.4% and 1.5%. Cyclist growth for the full year of 2024 is expected to be in the mid-teens on a year-over-year basis. Gross booking growth is expected to be slightly higher than year-over-year ride growth.

Adjusted EBITDA margin expansion is expected to be approximately 50 bps improvement year over year. It’s worth noting that the press release contained a typo regarding the adjusted EBITDA margin expansion, listed as 500 basis points when it was actually 50 basis points year over year. This sent stocks into a frenzied rally and then a pullback before resuming an uptrend.

CEO Insights

CEO Risher noted that the company expects to generate full positive cash flow in 2024 on an annual basis for the first time in its history. The company has prioritized its focus on drivers and has seen a 47% increase in driving hours year-over-year. The company also implemented a policy whereby drivers earn at least 70% of the rider’s weekly payments after external rates are applied. Lyft also saw significantly lower primetime year-over-year growth. Primetime is Lyft’s version of Uber’s price increases during busy periods. He’s noticed that people are getting out more when commuting, traveling and going to events.

CEO Risher concluded: “The headline is that in 2024 we expect Lyft to generate positive free cash flow on an annual basis for the first time in our company’s history. It’s a huge milestone for us. I’m very proud of all Lyft has caught up in 2023 and the first few weeks of 2024. As I said at the beginning, this will be the year we prove that customer obsession leads to profitable growth.”

Lyft analyst ratings and price targets can be found on MarketBeat. THE MarketBeat Stock Screener can help you find Lyft peers and competitor stocks.

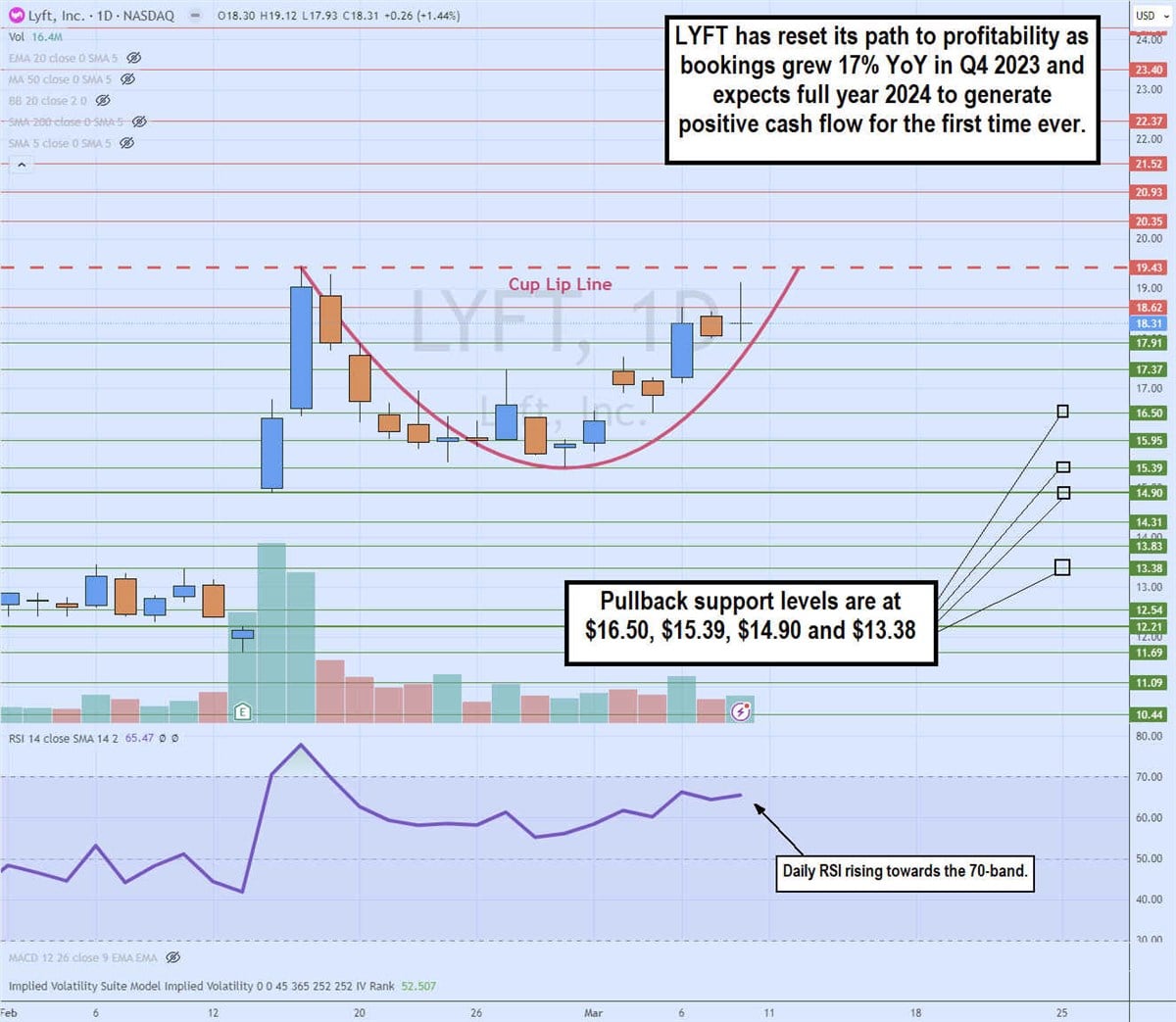

Daily mug template

The daily candlestick chart on LYFT illustrates a cup pattern. The cupped lip line formed at the peak of $19.43 formed on February 15, 2024, following its gap to $14.90 and short squeeze the next day to 52-week highs. Shares got a healthy pullback to the $15.39 level, forming a rounded bottom and holding above the gap-fill level at $14.90, setting the stage for a rally towards the cupped lip line for complete the cup pattern. The daily relative strength index (RSI) has steadily moved back towards the 70 band. The pullback support levels are at $16.50, $15.39, $14.90, and $13.38.

Before you consider Lyft, you’ll want to hear this.

MarketBeat tracks daily Wall Street’s highest-rated and best-performing research analysts and the stocks they recommend to their clients. MarketBeat identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market takes hold… and Lyft wasn’t on the list.

While Lyft currently has a “Hold” rating among analysts, top analysts believe these five stocks are better buys.

View the five stocks here

Wondering what the next big-hitting stocks with solid fundamentals will be? Click the link below to learn more about how your portfolio could blossom.

Get this free report