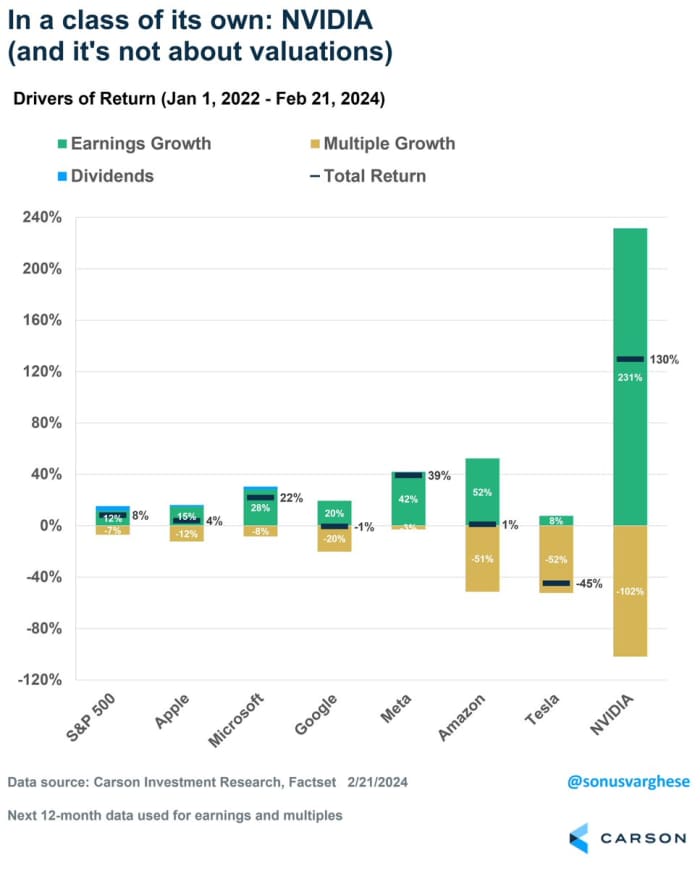

Nvidia’s spectacular growth is sometimes difficult to quantify.

But this chart, from Sonu Varghese, global macro strategist at Carson Group, helps put things in perspective.

Show as Nvidia’s NVDA,

earnings – or, to be more precise, analysts’ expectations of its earnings 12 months from now – have risen well above its share price, effectively leading to a multiple contraction of 102 points over the past two-plus years.

That’s not to say Nvidia is necessarily cheap, Varghese said in a message on the social media service X.

“There’s a trail here. Of course, how long can they continue to print profits like this… that is the question,” she said. “There is also operating leverage, with profits rising as sales grow. So margins are increasing.”

As MarketWatch’s Therese Poletti points out, Nvidia’s margins in the chip space are surpassed only by ARM Holdings ARM,

the microchip designer.

Nvidia shares rose 16% to $785.38 on Thursday, after the microchip maker beat fourth-quarter revenue expectations by about $2 billion, and also forecast first-quarter sales that midway through it will be almost 2 billion dollars more.

Nvidia is now ahead of both Amazon.com AMZN,

and GOOGL alphabet,

by market capitalization.

Over the past 52 weeks, Nvidia shares have risen 237.2%.